his period (August/September), I wanted to delve into the subject of GRI standards because I consider them a very important tool for assessing the starting performance and subsequently the improvement or deterioration of the activity we are analysing.

The Global Reporting Initiative (GRI) is an international non-profit organisation founded in 1997 in Boston to define standards for reporting on sustainable performance (also known as social reporting) of companies and organisations of any size belonging to any sector and country in the world.

The GRI standards are free of charge, usable by all and accompanied by explanations, only very specific courses are chargeable.

The standards are not very simple at first glance, but in my opinion, the best way to approach them is to

- analyse a document in which the standards are present,

- check that you understand the theory by following the different steps of the guidelines provided,

- test your understanding by starting to draft the report for your activity.

Currently, I am proceeding with the first two steps, the third point takes more time, and I want to do it for my hotel to get a practical approach.

The document I have decided to analyse is the ENEL sustainability report, not because I necessarily believe what it says, but because among those I have found available on the GRI website, it is one of the most understandable and written in Italian.

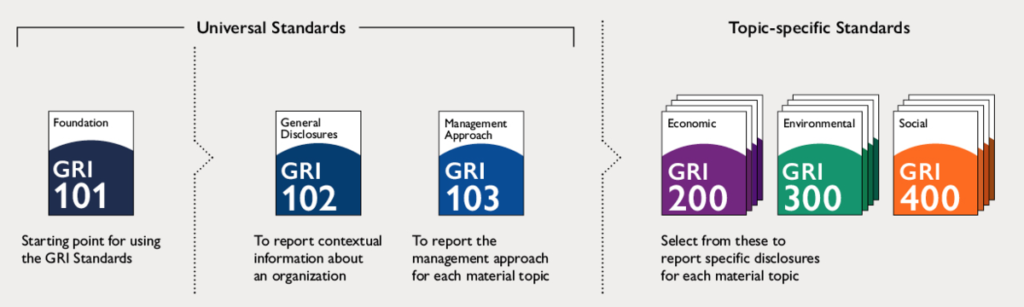

I start with the report’s structure to understand which GRI criteria are included. The complete file is available and can be downloaded here (scroll down to see the files ready for the download. https://www.enel.com/investors/sustainability

Structure of the report: part one

The first part of the report presents the typical elements that present the activity of a company.

- Title

- Letter to stakeholders (GRI 102-14 Statement by a senior manager)

- Summary Infographic

- Index

Company view (at a glance) includes:

The business model (resources, outputs) and value created

The governance of sustainability

ESG integrated into the business.

In this section, the GRI criteria found inside the report are

The criteria can be found online in Italian (2016 version for the moment) and English version 2020. Click here to download the version most appropriate for you.

Structure of the report: part two

The second, most information-intensive part, deals with ESG performance

Energy transition

NET ZERO AMBITION

A just and inclusive transition

Stakeholder engagement in the fight against climate change;

Enel’s climate advocacy activities;

Enel’s governance model to tackle climate change;

Enel’s impact on climate change

Climate scenarios

The strategy for tackling climate change

Main risks and opportunities related to climate change

Enel’s performance in tackling climate change.

ELECTRIFICATION, DIGITAL AND PLATFORMS

Operational excellence and quality in distribution

Service quality and promotion of responsible and conscious consumption

The centrality of people

OUR PEOPLE

Enel people around the world and the Open Power model;

Connected and close: smart working and caring during emergencies;

Investing in our people;

Listening and dialogue

Diversity and inclusion;

Gender gap and gender pay gap: our action plan

Caring for all

Supplementary healthcare and supplementary pensions

Industrial relations.

LOCAL AND GLOBAL COMMUNITIES

Strategy and shared value creation model

Value for countries and territories

Contribution to sustainable development objectives

The LBG method

Some examples of sustainability projects

Enel Heart

Access to energy

Main ongoing development projects and resettlement management

Growth accelerators

INNOVATION

Technologies and Innovability®

The Open Innovability® ecosystem

Innovating frontier technologies: Innovation Communities

Creating value in the future: intellectual property

Innovation starts with you: a new culture

The main programmes

DIGITAL MEDIA AND CYBER SECURITY

Digital Transformation

Cyber security

CIRCULAR ECONOMY

The governance of the circular economy

Circular activities of the Business Lines and main projects

Circular Open Meter

Targets and performance indicators

Circular City

Ecosystem involvement

A new circular culture

ESG foundations

SUSTAINABLE SUPPLY CHAIN

Purchasing and procurement of goods and services

Fuel procurement

OCCUPATIONAL HEALTH AND SAFETY

The health and safety system

Performance 2020

Safety in procurement processes

Infrastructure safety and technological innovation

Health

Development of safety culture: training and information

Safety of communities and third parties

Emergency management

Nuclear policy

Industrial relations on health and safety issues

ENVIRONMENTAL SUSTAINABILITY

Environmental governance

Emissions

Energy

Water

Waste

Soil, subsoil and groundwater

Biodiversity

ROBUST GOVERNANCE

Corporate governance model.

In this section, the GRI criteria are answered according to the ENEL report

102-5 102-7 102-9 102-10 102-11 102-12 102-13 102-15 102-16 | Ownership and legal form Size of organisation Su |

Structure of the report: part three

Part Three sets out the Trend Topics

FISCAL TRANSPARENCY: APPROACH TO TAXES

Tax governance, control and risk management

Transparent stakeholder relations

Reporting

The European Taxonomy

Green Bond Report 2020 – accompanying notes

In this section, the GRI criteria are answered according to the ENEL report

207-1 Approach to taxation

207-2 Fiscal governance, control and risk management

207-3 Stakeholder engagement and management of tax concerns

207-4 Country-by-country reporting.

The fourth part consists of the appendix. This section contains the indices as well as the methodological note and the auditors’ report and sustainability performance indicators.

- methodological note and the auditors’ report

- How this document was constructed

- Analysis of the 2020 priorities

- Identification of issues and stakeholders

- Allocation of priorities to stakeholders

- Evaluation of theme priorities assigned by stakeholders

- Evaluation of theme priorities in corporate strategies in relation to impacts generated

- Linking the themes in the priority analysis to the GRI Standards.

- The reporting process

- Drafting and assurance

- Report parameters.

- Sustainability statement: the performance indicators.

The key indicators are shown in the table as a fundamental part and consequently cover the same topics as the second section. In addition to this, there are indices for all the criteria used:

- GRI Content Index

- SASB Content Index

- TCFD Content Index

- WEF Content Index.

| 101 | Reporting principles for following the basic process for preparing a sustainability report |

| 102-1 102-3 102-5 102-10 102-32 102-40 102-42 102-43 102-45 102-46 102-47 102-48 102-49 102-50 102-51 102-52 102-53 102-54 102-55 102-56 | Name of organisation Location of head office Ownership and legal form Significant changes in the organisation and its supply chain Role of the highest governance body in sustainability reporting List of stakeholder groups Identification and selection of stakeholders Ways to engage with stakeholders Stakeholders included in the consolidated financial statements Defining Report Content and Topic Perimeters List of Material Issues Review of disclosures Changes in Reporting Reporting Period Date of most recent report Reporting Periodicity Contact information for inquiries regarding the report Statement on reporting in accordance with GRI Standards Index of GRI content External Assurance |

| 103-1 | Explanation of material topic and boundary |

Some important general indications

For the criteria mentioned, we always find similar indications

102-2 Activities, brands, products and services

The organisation must report the following information

- a description of the organisation’s activities

- the main brands, products and services, including an explanation of any products or services that are prohibited in certain markets.

Reporting recommendations

1.1 In reporting the information specified in Statement 102-2-b, the organisation should also explain whether it sells products or services that are the subject of stakeholder or public debate.

This is because as required by the “defining the content of the report” guidelines there are some basic principles of proper content for the report:

- Relevant topics identified by involving stakeholders;

- Assess the relevance of the indicators for the identified topics;

- Use available tests to understand whether we have said everything, i.e. whether the information is complete;

- The principle of prioritisation should be used to establish the importance and order of inclusion of topics;

- The methods and processes used to assess relevance must:

- Be specific and customisable for each organisation;

- Always take into account the instructions and tests included in the reporting principles.

The best approach in my opinion is to start from the existing report, if any, or to work by drafts taking inspiration from those who produce one. For this motive I wanted to include the latest available ENEL report.

A comparison with the index of your activity report can immediately indicate if there are topics that you have not included at all. Understanding why this inclusion was not there is very important to assess how to improve it and how to integrate it with the GRI criteria.

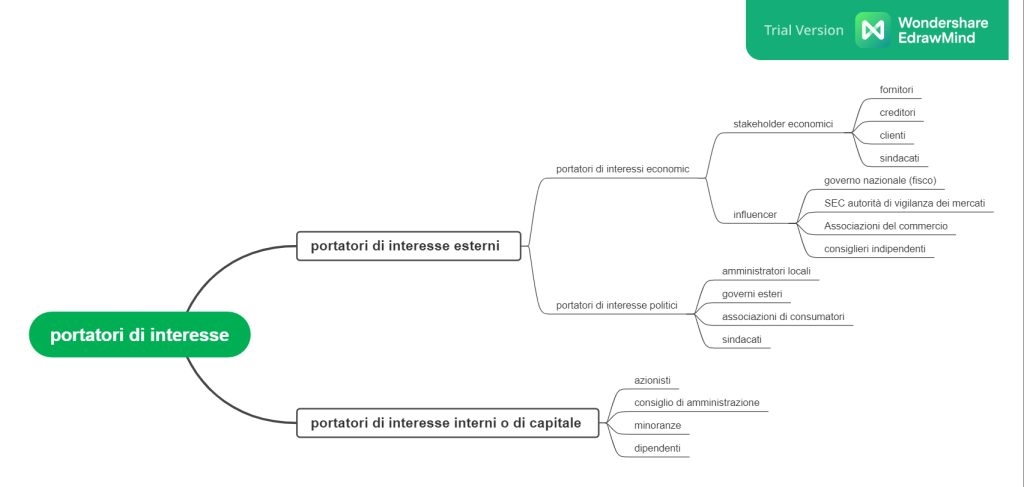

Suppose you take the first steps in writing the report for your business. In that case, the GRI criteria provide a very useful indication: indicate for whom the report is mainly intended and report 60/70% of the useful information for these people (for this target group). In general, these are the stakeholders who invest in the business (investors, shareholders, customers, employees); the remaining information included 30/40% should concern the non-direct stakeholders or more generally those with a less direct interest but who have every right to know and be aware of the company’s improved or worsened impacts (positive or negative). They can be, for example, communities and residents of the area where the company’s activities take place.

In the case of Hotel Loveno accommodation SNC, the direct stakeholders are:

Shareholders: Paolo and I, our family ;

Customers: Our guests;

Employees: our employees.

Non-direct stakeholders:

PromoMenaggio Association to which we are members and contributed to restoring during 2020 and 2021.

The municipality of Menaggio considers only the payments made to the municipality for waste disposal, the contribution paid through the tourist tax by our guests and by ourselves as a business.

Residents of Menaggio may benefit indirectly from our activity: businesses and restaurants for example, potential new customers. A bar open in the Loveno area for those passing through. Job opportunities and/or seasonal collaboration. A potential sponsor for social, recreational, or ecological activities close to our sensibility.

Working on a GRI report takes time and energy, so this is one of my goals for the 2023 season at the hotel.

Main source of information in English

Global Reporting https://www.globalreporting.org/standards

https://www.globalreporting.org/media/ukgpbiqx/linking-the-gri-standards-and-cass-csr-40-english.pdf

Sara – tourism sector consultant

Did you know that even the corporate world has been moving towards a more sustainable approach for some years?

I am Sara, a consultant for the tourism sector, and on this site, I talk about tourism, sustainability, theory and practical ways to become a more sustainable operator.

Before you continue, subscribe to the newsletter if these topics interest you! So you won’t miss a single update.

Today’s topics

– CSR: corporate social responsibility introduction and considerations;

– From ethical principles to ESG (Environment, Social, Governance) model;

– Social and Environmental Reporting.

Through years of studying, working and understanding sustainability in tourism, I have realised how important it is to have benchmarks and guidelines that can help businesses of all levels find ways to achieve their sustainability goals.

This need led me to expand my horizons at first in the international sense of the criteria for the sector. So I studied and understood the GSTC criteria. The GSTC council is an international organisation of the tourism sector that provides the basis for assessing whether the sector’s certifications meet minimum standards and promote a truly sustainable approach to tourism.

A few weeks ago, I approached, so far from a theoretical point of view, the corporate world. I have come across topics I have already seen (such as GRI standards) and have been able to delve into corporate social responsibility. I chose this direction because I believe it is one of the best ways to go against greenwashing and have a few more tools to evaluate larger companies and their strategies.

My primary source of information is Italia and is the book Communicating Sustainability, Beyond Greenwashing by Professor Aldo Bolognini Cobianchi.

Corporate Social Responsibility definition and considerations

Corporate Social Responsibility concerns ethical implications within the strategic business vision in economic and financial terminology. It is a manifestation of the willingness of large, small and medium-sized enterprises to manage social and ethical impact issues within their business effectively and in their areas of activity.

The behaviour demanded of the company is what is known as socially responsible. It is considered not only the legal responsibility of the company but a responsibility that involves vast swathes of subjects who, although they are not owners of shares, have a de facto interest in participating in the management of the company itself (the so-called stakeholders).

Corporate social responsibility can be said to involve two different dimensions: the internal dimension within the company, i.e. the attention that must be paid to its human resources, and the external dimension, i.e. the attention paid to the outside world, i.e. the relationship with the local community, business partners, consumers, suppliers and the environment in general.

Regarding the first aspect, CSR requires that the company guarantees fair pay and career opportunities for women and men (without discrimination), the hiring of disadvantaged groups, the possibility of training staff throughout their working careers, and finally, an essential element, safety in the workplace.

The relationship with the rest of the world lies in guaranteeing respect for the environment in which it operates. Therefore, the company should favour where it conducts its activities by developing local professionalism and protecting the environment (reducing the polluting impact).

Altogether, the people involved forming the set of stakeholders.

The relationship with stakeholders is mainly based on ethical grounds, i.e. on moral obligations, the company imposes on itself to meet their legitimate expectations.

There is (as yet) no law that requires the expectations of all the different categories of stakeholders to be met, although some of these are regulated by law: for example, the obligation to compensate shareholders, to pay employees and collaborators, to pay suppliers, to give customers products that conform to the promised characteristics, to pay taxes to the state and local authorities, and so on.

Ethical codes, ESG model and sustainability reports

Other obligations derive from contractual clauses. But, in general, what governs the whole matter are the moral obligations to which the company agrees to submit to be responsible and thus sustainable.

But where are these ethical bases written down? They are usually laid down in policy documents called codes of ethics.

In these codes, the company or organisation that draws them up describes everything it undertakes to do (or not to do) about the different categories of stakeholders.

Codes are not binding; they are voluntary, non-binding, or soft law. Nobody obliges companies or organisations to follow what is stated. In addition, there are no tools to measure their actual application objectively.

On the other hand, there are forms of certification of the application of different soft law standards (such as ISO standards), i.e. internal company rules that can be imposed as contractual clauses. One example is firing an employee who does not comply with the ethical regulations expressed in the employment contract or terminating relations with suppliers who do not comply with the ethical standards set by the company, provided that these are made explicit in the supply contracts.

There are also criteria for ethical standards that apply to everyone because the market has given itself criteria. These criteria are called ESG and cover three factors: environment, social (responsibility), and governance, the three criteria on which sustainability is based. The ESG criteria originated in the financial market to allow investors to define the degree of sustainability of a company or security. The criteria originated in the 1970s and 1980s. Since 2008, they have become firmly established to replace the previous standards that determined the decision to invest in security, which was undermined by the crisis.

There is only one historical difference between environmental, social and sustainability reporting.

The environmental report was born first in the 1980s. It was absorbed by the social report in the 1990s and was supplanted by the sustainability report in the mid-2000s.

Currently, only non-profit companies and cooperatives continue to produce social reports due to these types of companies’ more humanitarian and solidarity-oriented direction. However, among non-profit organisations, third sector entities (ETS) are obliged to have a social report if they exceed certain size thresholds.

Organisations and international initiatives for corporate social responsibility

On a supranational and global level, the initiative most worthy of mention is the UN Global Compact.

This is a network of national and international organisations from the world’s regions, recommended by the UN Secretary-General in Davos in 1999.

The network aims at the realisation of two objectives: the first is related to the willingness of the company to integrate the principles of the Global Compact into its internal structure; the second is to involve different stakeholders in the cooperation and resolution of rather significant issues. The overall goal is to be able to create a ‘more sustainable and inclusive market.

The principles that the Global Compact recognises as indispensable are:

- Human Rights

- Labour

- Environment

- Fight against corruption.

The first initiative the OECD took on this subject dates back to 1976 when the Guidelines for Multinational Enterprises were first adopted. However, this document has gained more relevance recently, as it was revised in 2000, making it more relevant to the issues affecting enterprises and their socially responsible management.

According to the European Union, a socially responsible company aims to meet the customer’s needs and contribute to society’s needs.

In 2001 the European Commission published a document, the so-called Green Paper, “Promoting a European Framework for Corporate Social Responsibility”, on corporate social responsibility as a form of support for all companies.

It followed the work of the Lisbon Conference in 2000, where the new European Employment Strategy was defined and promoted for the first time.

This document resulted in the Communication on ‘Corporate Social Responsibility: A business contribution to Sustainable Development. It proposes a balanced strategy to develop different CSR instruments, including integrating corporate social

Organisations and international initiatives for corporate social responsibility

On a supranational and global level, the initiative most worthy of mention is the UN Global Compact.

This is a network of national and international organisations from the world’s regions, recommended by the UN Secretary-General in Davos in 1999.

The network aims at the realisation of two objectives: the first is related to the willingness of the company to integrate the principles of the Global Compact into its internal structure; the second is to involve different stakeholders in the cooperation and resolution of rather significant issues. The overall goal is to be able to create a ‘more sustainable and inclusive market.

The principles that the Global Compact recognises as indispensable are:

- Human Rights

- Labour

- Environment

- Fight against corruption.

The first initiative the OECD took on this subject dates back to 1976 when the Guidelines for Multinational Enterprises were first adopted. However, this document has gained more relevance recently, as it was revised in 2000, making it more relevant to the issues affecting enterprises and their socially responsible management.

According to the European Union, a socially responsible company aims to meet the customer’s needs and contribute to society’s needs.

In 2001 the European Commission published a document, the so-called Green Paper, “Promoting a European Framework for Corporate Social Responsibility”, on corporate social responsibility as a form of support for all companies.

It followed the work of the Lisbon Conference in 2000, where the new European Employment Strategy was defined and promoted for the first time.

This document resulted in the Communication on ‘Corporate Social Responsibility: A Business Contribution to Sustainable Development.

It proposes a balanced strategy to develop different CSR instruments, including integrating corporate social responsibility into all EU policies.

In Italy, the implementation of strategies to integrate the concepts of Corporate Social Responsibility is mainly left to the government, particularly the Ministry of Labour, which has set up a Multi-stakeholder Forum.

The objectives that the Ministry proposes to achieve are:

- to develop those practices that favour the dissemination of the CSR culture;

- that enable the evaluation of the performance of companies in this area;

- and that aims to support SMEs, representing our entrepreneurial system’s substratum.

The realisation of these objectives is also supported by encouraging the exchange of experiences with other countries to be able to apply the best practices already found internationally.

The ‘CSR Forum‘ (Italian Multi-Stakeholder Forum for Corporate Social Responsibility) was established, which aims precisely to put government intentions into practice through a series of initiatives to raise awareness of the importance of the relationship between CSR and sustainable development.

Sources

- Comunicare la sostenibilità, oltre il green washing. Aldo Bolognini Cobianchi.

- https://sustainabilityaward.it/che-cosa-e-la-responsabilita-sociale-dimpresa/;

- https://www.fondazionenazionalecommercialisti.it/system/files/imce/aree-tematiche/pac/ET_RSI_%20ETICA.pdf;

- https://coopthc.org/la-responsabilita-sociale-dimpresa-cose-principi-e-vantaggi/;

- https://www.contributipmi.it/responsabilita-sociale-di-impresa/

There is quite a misunderstand online regarding this subject, I hope to clear meaning with some definition (from United Nations website) and example from Spain.

Corporate Social Responsibility (CSR) as defined by United Nation

• The Corporate Social Responsibility (CSR) is the voluntary commitment that companies make for social, economic and environmental improvement.

• The CSR wants to go beyond compliance with laws and regulations, assuming its respect and strict observance. The concept of administration and management encompasses a set of practices, strategies and business management systems which seek a new balance between economic, social and environmental dimensions.

• CSR is synonymous of transparency of investors, of good governance of listed companies, codes of ethics, initiatives of social actions and cultural patronage, among other initiatives. Social organizations develop their mission, establishing at the same time communication channels with the Administration and companies.

The reason why I choose to share info about Corporate Social Responsibility is the United Nations Association has found the Global Compact, in Spain, a strategic policy initiative for businesses that are committed to aligning their operations and strategies with ten universally accepted principles in the areas of human rights, labour, environment and anti-corruption. It is the largest voluntary corporate responsibility initiative in the world.

The Global Compact is a practical framework for the development, implementation, and disclosure of sustainability policies and practices, offering participants a wide spectrum of workstreams, management tools and resources — all designed to help advance sustainable business models and markets.

Read more about The Global Compact: https://www.unglobalcompact.org/aboutthegc/TheTenprinciples/index.html

How the Corporate Social Responsibility is applied?

Marco de Comunicacion is a Spanish agency of communication working with many corporate in differentes sectors, they also promote their clients’ corporate values and develop impactful Corporate Social Responsibility (CSR) plans. The clients are different, in some cases, CSR is part of the company’s corporate philosophy, while for others, CSR has even further-reaching implications.

The examples I like most:

MdC managed Spain’s first solidarity cooking marathon, an event held as part of a corporate social responsibility campaign for BEKO Home Appliances. The event was supported by Caritas and Madrid City Council, among others.

For a client such as Prologis, operating in the logistics, transportation and construction sectors, CSR has become a way to give back to the community. MdC designed a powerfulcommunications plan which reinforced Prologis’s green approach as a model for repairing the sector’s impact on the environment. The strategy implemented by MdC helped communicate Prologis’s use of recycled and renewable materials in its installations and positioned the company as one of the pioneers in sustainability in the Spanish logistics sector.

MdC created a communications plan for The Body Shop, the only ethically concerned beauty brand, to re-launch it to Spanish consumers after it was bought by L’Oreal. Thanks to the six-month PR campaign implemented by MdC, The Body Shop successfully re-positioned itself as an ethically concerned brand, reaching an audience of more than 115 million with 142 media appearances.

Resource:

1. http://www.anue.org/en/content/social-responsibility

2. http://www.marcodecomunicacion.com/en/servicios/corporate-social-responsibility/

Interested on Corporate Social Responsibility?

Stay tuned, the best is yet to come!

Sara