I participated in the Mediterranean Forum on Sustainable Tourism in Vietri sul Mare (Amalfi Coast). The conference was organized by Propellers International Club, an association of maritime sector operators from all levels of the industry.

Among the participants were:

Policy makers and regulators

- Ministries and national government

- Maritime authorities

- Port authorities

- Regional and local governments

Economic operators with direct impact

- Port terminals

- Shipping companies and maritime transport operators

- Marinas and nautical sector

System influencers (associations and clusters)

- Maritime associations

- Economic clusters and networks

Tourism and territory

- International organizations

Scientific community and civil society

- Research institutions and universities

- Environment and biodiversity organizations

- Maritime culture organizations

The presence of so many stakeholders allowed me to learn more about the sector and to better understand its internal and external dynamics, which are often difficult to grasp for those coming from a different field, whether through study or professional experience.

It was a very interesting opportunity to learn, reflect, and analyze several important topics. In this article I try to give a logical structure to the insights that emerged from participating in the Forum.

- Why is the maritime sector today under strong regulatory pressure and why has change become mandatory even though it accounts for only 3–5% of global emissions?

- How does the maritime sector contribute to pollution?

- What does the “green transition” mean in the maritime sector? What are the objectives to be achieved?

- What are the Motorways of the Sea, and why do some maritime operators refer to them as the green solution of the 1990s?

- What are the real challenges in improving the sector?

- What actions are currently underway and what progress has been made? What is the current situation in Italy?

Why is the maritime sector (cargo + cruise) today under strong regulatory pressure?

The European Commission’s Green Deal

The European Union has very ambitious targets for:

- climate neutrality by 2050

- a significant reduction in greenhouse gases and pollutants

Because maritime transport operates on a very large scale globally, even though it is energy-efficient per tonne-kilometre, the overall volume of emissions remains too high relative to climate targets.

For many years, maritime transport remained largely outside the major climate policy frameworks. The sector was long exempt from strict emissions regulations and relied on low-cost fossil fuels.

This de facto exclusion lasted roughly 20–30 years, with relatively slow progress from the early 1990s until the more recent agreements (2018–2023) aimed at maritime decarbonization.

European regulations and instruments

- FuelEU Maritime introduces limits on the carbon intensity of marine fuels and encourages the use of low- and zero-carbon fuels.

It requires:

- progressive reduction in the carbon intensity of fuels

- mandatory use of shore power (cold ironing) for passenger ships while at berth.

- Emissions Trading System (ETS) From 2025, maritime transport will be included in the EU Emissions Trading System, requiring companies to pay for the CO₂ they emit.

The ETS sets a cap on total emissions, which decreases each year to push industries to pollute less.

Shipping companies must purchase CO₂ allowances for:

- 100% of emissions from intra-EU routes

- 50% of emissions from routes between EU and non-EU ports

This gives emissions a real economic price, as already happens in other sectors.

Revenues generated from the auctioning of allowances are reinvested by Member States in strategic areas.

In Italy, GSE manages the auctions, and a significant share of the revenues is legally earmarked to support renewable energy incentives.

- Stricter limits on SOx, NOx and PM. New restrictions on sulfur oxides (SOx), nitrogen oxides (NOx), and particulate matter (PM) are being introduced in emission control areas.

From 2025, the Mediterranean becomes a Sulfur Emission Control Area, with sulfur content limited to 0.1%.

This significantly reduces:

- sulfur oxides

- particulate matter

- health impacts in coastal areas.

Innovation and market forces

Traditional fuels such as heavy fuel oil are among the most polluting and are becoming less economically competitive.

Financial incentives and investments in green solutions—such as port electrification, hydrogen, and ammonia fuels—are therefore becoming increasingly important.

Sources & insights

Why is change required for a sector responsible for “only” 3–4% of emissions?

3–4% is not insignificant in climate policy

The EU must reduce emissions by about 55% by 2030 compared with 1990 levels.

When every sector must drastically cut emissions, there are no longer any “negligible shares”. If every sector claimed “we are only 3%”, climate neutrality would be impossible.

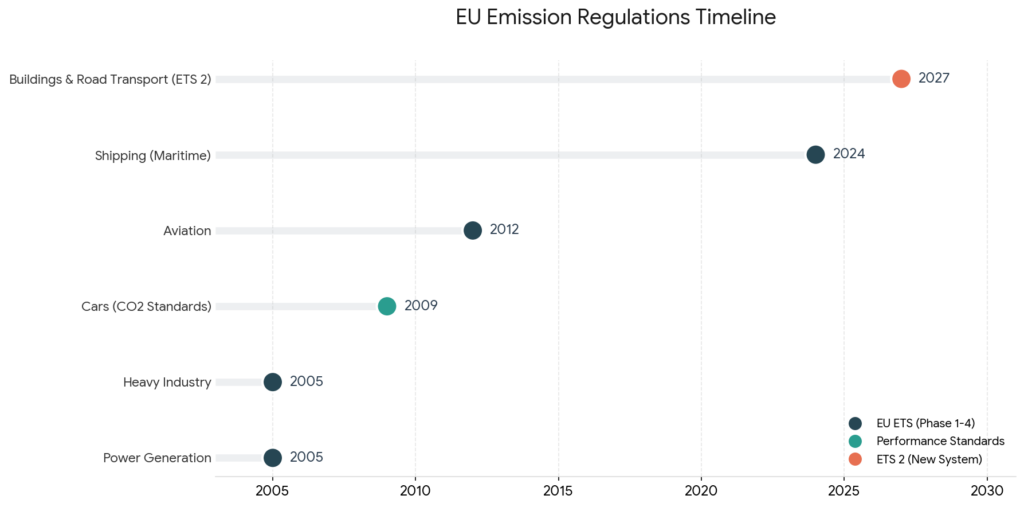

It was one of the last unregulated sectors

For many years:

- Industry → ETS since 2005

- Energy → ETS since 2005

- Aviation → ETS since 2012

- Cars → CO₂ standards since 2009

Maritime transport remained outside the ETS. Therefore, today’s regulation is not a punishment, but a regulatory alignment.

Projected growth in emissions

According to the International Maritime Organization, maritime emissions could increase by up to 50% by 2050 without intervention.

Strong local impact in port cities

While 3–4% refers to global CO₂ emissions, the sector has strong local impacts on:

- NOx

- SOx

- particulate matter

- urban air quality in port cities.

Cities such as Venice, Barcelona, and Marseille are facing strong political and public health pressure.

Technology is becoming available

Emerging solutions include:

- LNG (Liquefied Natural Gas),Methanol,Ammonia (under development),Hydrogen

- Port electrification

The EU therefore considers the sector technically transformable.

Carbon pricing

With the ETS:

- inefficient ships become more expensive

- investing in efficiency becomes economically rational.

Social and tourism pressure

In the Mediterranean:

- cruise ships are often perceived as highly polluting

- tourist cities increasingly demand limits.

How does the maritime sector pollute?

Maritime transport is a significant source of emissions, particularly on international routes.

Greenhouse gases

- CO₂ – the main greenhouse gas from fossil fuels

- CH₄ (methane) – increasing due to LNG use

Local air pollutants

- SOx – cause acid rain and respiratory problems

- NOx – contribute to smog and tropospheric ozone

- PM – harmful to human health near ports and busy routes.

Other environmental impacts

- Water pollution – wastewater discharge, fuel washing residues, oils

- Underwater noise – disturbing marine wildlife

- Invasive species – transported through ballast water.

What does the “green transition” mean in the maritime sector?

The green transition in the European maritime sector refers to the mandatory decarbonization process aimed at achieving net-zero emissions by 2050, in line with the European Green Deal and the Paris Agreement.

The EU and its Member States committed to limiting global warming to +1.5°C compared to pre-industrial levels.

As part of the European Green Deal, the EU has committed to achieving climate neutrality by 2050, with an interim target of reducing greenhouse gas emissions by 55% by 2030.

This means replacing fossil fuels with sustainable alternatives (hydrogen, ammonia, green methanol), improving the energy efficiency of ships and adopting zero-emission technologies.

In the next 15–20 years we are likely to see:

- dual-fuel vessels

- green methanol

- hydrogen for short routes

- mandatory shore power in ports

- digital efficiency solutions (AI routing, slow steaming)

- revised cruise industry business models.

Sources and Insights

Motorways of the Sea (1990s–2000s)

In the 1990s Italy promoted the concept of Motorways of the Sea, later integrated into the TEN-T European transport network.

The main objectives were:

- reducing congestion on highways (especially Tyrrhenian and Adriatic corridors)

- improving logistics competitiveness

- reducing road accidents and congestion.

The environmental benefit was indirect.

Maritime transport is more efficient than trucking in terms of emissions per ton-kilometer, which means:

- lower CO₂ emissions per ton transported

- fewer NOx and particulate emissions compared with thousands of trucks over long distances.

However, the policy was primarily logistical and infrastructural, not climate-driven.

One could therefore argue that this strategy was appropriate for Italy in the 1990s and early 2000s, but today—in 2025–2026—we have the opportunity to go further.

The regulations are European rather than Italian because we have chosen to be part of a union that protects key interests such as the free movement of goods, people, services and capital.

Being part of the EU also benefits the maritime sector itself.

At the same time, it requires managing regulatory frameworks that may involve significant and sometimes costly changes.

Sources and insights

Italian ministry for transport https://www.mit.gov.it/en

https://www.ramspa.it/sites/default/files/2025-12/rapporto-di-ricera_autostrade-del-mare.pdf

What are the real challenges for improving the sector?

The main criticisms raised by the industry are not only about whether change is necessary, but about the practical challenges of implementing it.

Major concerns come from shipping associations such as:

- European Community Shipowners’ Associations

- International Chamber of Shipping

- CLIA

In Italy:

- Confitarma

- ALIS.

Risk of loss of global competitiveness

The EU has introduced much stricter rules than many other regions.

The concern is that:

- shipping is a global industry

- about 50% of EU routes involve non-EU ports

If only the EU prices emissions, it could create a competitive disadvantage.

Shipping companies fear traffic could shift to non-EU ports (e.g., North Africa or Turkey).

Carbon leakage concerns

European operators argue that strict EU regulations could favor non-EU operators or ports with lower regulatory costs.

The EU is trying to address this risk through instruments such as the Carbon Border Adjustment Mechanism (CBAM).

This is an attempt to balance environmental goals with economic competitiveness.

Limited availability of alternative fuels

Shipping companies argue that:

- green methanol is not available at sufficient scale

- green ammonia is still in pilot phase

- hydrogen is logistically complex.

Prices are 2–5 times higher than traditional fuels.

The industry therefore criticizes policies that require fuels that are not yet available at industrial scale.

The EU, however, is investing heavily through programs such as Horizon Europe and the Innovation Fund.

High costs and short timelines

Ships typically have a lifespan of 20–30 years.

Many current vessels:

- were built before the Green Deal

- are difficult to convert.

Retrofitting is expensive and new dual-fuel ships cost 20–40% more.

This creates the risk of stranded assets, meaning ships or port infrastructure losing economic value before the end of their useful life.

Double regulation (EU vs IMO)

Shipping is a global industry and the International Maritime Organization (IMO) already has a climate roadmap.

However, the EU is moving faster than the global framework.

According to operators this creates:

- regulatory fragmentation

- administrative complexity

- double reporting requirements

- regulatory uncertainty.

The industry would prefer a single global regulation.

Impact on consumers and inflation

About 75% of EU external trade moves by sea.

Shipping operators argue that:

- ETS + green fuels will increase logistics costs

- imported goods may become more expensive.

In the cruise sector, CLIA also argues that:

- costs will be passed on to passengers

- some ports may receive fewer cruise calls.

Additional concerns include:

- shore power not yet available in all ports

- port infrastructure investments not aligned with ship investments

- strongly negative media narratives.

In Italy, some analyses indicate an increase of about 45% in the “equivalent fuel price” linked to ETS costs compared with previous levels.

Consumer associations have raised concerns that ticket surcharges for ferries or freight transport may not always be transparent, potentially leading to antitrust scrutiny.

Summary: criticism vs policy response

Industry criticism | How valid it is | Policy / industry response |

High ETS costs | Strongly grounded | ETS revenues reinvested in transition |

Alternative fuels not ready | Grounded | Funding and pilot projects |

EU competitiveness | Partly grounded | CBAM and global dialogue |

Administrative complexity | Grounded | MRV standards already harmonized |

Consumer price increases | Debated | Competition oversight and ETS redistribution |

Many analysts note that the sector does not contest the climate objective itself, but rather the timing, implementation methods, and the unilateral pace of the EU.

In other words:

It is not “we do not want to become green.”

It is “not like this, not this fast, and not only us.”

The second part of this article, to be published shortly, answers the question: ‘Where are we today?’ Where does Italy stand?